Profile

Structure

Easypaisa Bank Limited (formerly Telenor Microfinance Bank Limited) ("Easypaisa" or the "Bank") is incorporated in Pakistan as a public limited company and is engaged in digital banking and related services. On 28 January 2025, the Bank has been granted commercial license for Digital Retail Bank from the State Bank of Pakistan and declared as scheduled bank under the SBP Act, 1956.

Background

Telenor Microfinance Bank Limited, Easypaisa, was incorporated on August 1, 2005, under the Companies Ordinance, 1984 (now Companies Act, 2017) with SECP, and commenced operations in September 2005. Easypaisa was one of five contenders for a digital retail bank license under Pakistan’s Digital Banks Framework 2022, committed to financial inclusion. In the evolving digital landscape, the Bank — by virtue of its operational history and well-designed business strategy — was exempted from pilot and transition phase and restrictions on deposit and lending. This transition marks a defining moment in the Bank’s journey, reaffirming its position as a leader in Pakistan’s digital landscape. The Bank's registered office is situated at 19-C, 9th Commercial Lane Main Zamama Boulevard, Phase V, DHA, Karachi.

Operations

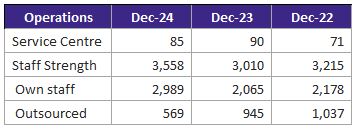

As part of its digital transformation, Easypaisa streamlined its branch network, reducing it to 25 full-service locations, while converting the remaining branches into cashless service centers. As a leading player in the digital banking space, the Bank continues to drive innovation, particularly in credit technology. On the lending front, Easypaisa continues to scale lending and has introduced a range of embedded finance solutions, including Buy Now, Pay Later (BNPL) options for airtime and utility bill payments, as well as Merchant Cash Lending, significantly improving credit access for individuals and small businesses. These offerings are expected to be further expanded in 2025 to strengthen credit accessibility across underserved segments. In addition, the Bank has launched several innovative savings and investment products designed to cater to the evolving needs of its diverse customer base. These include Savings Pockets, Daily Savings Plans, and Digital Term Deposits, all of which have contributed meaningfully to the growth of Easypaisa's savings portfolio. Looking ahead, the Bank is preparing to launch new offerings such as international remittance services, freelancer digital accounts, Roshan Digital Accounts, and e-commerce integrations, aimed at further broadening its product suite and reinforcing its position as a comprehensive digital financial services provider.

Ownership

Ownership Structure

Easypaisa Bank Ltd is a joint venture between Telenor Pakistan B.V., a public limited company headquartered in Amsterdam, Netherlands, holding a 55% majority shareholding, and Alipay (Hong Kong) Holding Limited, holding a 45% shareholding. Telenor Pakistan B.V. is a subsidiary of Telenor ASA, a Norwegian telecommunications company, while Alipay (Hong Kong) Holding Limited is a subsidiary of Ant Group Co., Ltd., a Chinese financial technology company.

Stability

Ant Group is an affiliate company of the Chinese conglomerate Alibaba Group. The group owns the world's largest mobile payment platform Alipay, which serves a huge number of users across the world. Telenor ASA, the parent company of the Telenor Group is a subsidiary of the Government of Norway. It is one of the world’s major mobile operators, headquartered in Oslo, Norway, with operations across 8 countries.

Business Acumen

Ant Financial is one of the world’s leading fintech conglomerates, known for its innovation and scale in digital financial services. Easypaisa is well positioned to benefit from Ant Financial’s strategic vision, technological expertise, and global experience. Similarly, Telenor Group, a prominent telecommunications provider with a strong footprint across the Nordics and Asia, brings deep expertise in connectivity and customer-centric digital solutions, further strengthening the Bank’s foundation for growth and innovation.

Financial Strength

The unwavering support of shareholders, Telenor Group, and Ant Group has been key to success with strategic investment of USD 319 million till 2024. In addition to the series of injections, Easypaisa lately secured a US$ 10 million equity investment from its shareholders, with ownership proportions remaining unchanged.

Governance

Board Structure

Overall control of the Bank vests with eight members of the Board of Directors, including the CEO. There are three independent directors, one executive director, and four non-executive directors, including the Chairperson, Mr. Irfan Wahab Khan, represent the Telenor Group. The Board has five committees: (i) People Committee, (ii) Audit Committee, (iii) Risk Management Committee, (iv) Information Technology Committee, and (v) Compliance Committee. In CY24, the Board held six meetings, with satisfactory attendance.

Members’ Profile

Mr. Irfan Wahab Khan – Chairman of the Board

Mr. Irfan Wahab Khan serves as the Chairman of the Board of Easypaisa Bank Limited and is also the Senior Vice President – Head of Portfolio Development at Telenor Group. He was formerly CEO of Telenor Pakistan (2016–2023), EVP and Head of Emerging Asia Cluster at Telenor Group, Chairman of Telenor Myanmar, and Director on the Board of Grameenphone. Since joining Telenor in 2004, he has held various leadership positions. He holds advanced degrees and certifications from the University of Westminster, Harvard, INSEAD, London Business School, and IMD Switzerland.

Mr. Henning Thronsen – Non-Executive Director

Mr. Thronsen serves as Head of Project & Corporate Finance at Telenor Group Treasury. He brings over 20 years of experience in finance, capital structuring, and M&A. He leads key strategic initiatives and holds board positions across Telenor entities.

Mr. Zhi Xian Li – Non-Executive Director

Mr. Li is Country Manager for Pakistan at Ant Group, managing partnerships and joint ventures. He has held leadership roles at China UnionPay, including as General Manager for Africa. He holds a Master’s in Computer Science from Ocean University of China.

Mr. Amjad Waheed – Independent Director

Mr. Waheed is CEO of NBP Fund Management Limited with over 30 years in investment banking and asset management. He previously managed equity funds at Riyad Bank, Saudi Arabia. He holds an MBA, PhD in Finance, and is a CFA charterholder.

Mr. Douglas Feagin – Non-Executive Director

Mr. Feagin is SVP at Ant Group, leading global partnerships and investments. Prior to Ant, he spent 20+ years at Goldman Sachs, focusing on finance and fintech. He holds a BA in Economics from UVA and an MBA from Harvard Business School.

Ms. Musharaf Hai – Independent Director

Ms. Hai has over 30 years of leadership experience, including CEO roles at Unilever and L’Oréal Pakistan. She also led Citigroup’s Consumer Bank in Pakistan. Her expertise spans multinational business development and market expansion.

Mr. Muhammad Shoaib – Independent Director

Mr. Shoaib is a Managing Director and Partner at BCG, with expertise in digital strategy, transformation, and cybersecurity. He has worked across finance and telecom sectors, including Celcom Axiata. He holds dual Master’s degrees from Charles Sturt University.

Board Effectiveness

The Board, drawing on extensive expertise in the financial and telecom industries, offers strategic counsel to the Bank and conducts regular

evaluations of management performance, including the assessment of growth targets.

Transparency

EY Ford Rhodes Chartered Accountants are the external auditors of the Bank. They expressed an unqualified opinion on the financial statements of the

bank for the year ended December 31, 2024.

Management

Organizational Structure

The Bank has eleven departments, each led by a department head who reports to the CEO. The head of internal audit reports to the Audit

Committee. The Senior Management team brings significant experience to their roles.

Management Team

Jahanzeb Khan – President & CEO

Appointed in July 2024, Mr. Khan brings over 25 years of global experience in digital banking and fintech. He has held leadership roles at Finca, JP Morgan, and Deloitte. His expertise includes digital solutions, payments, and strategic transformation. Known for driving revenue growth through innovation and operational excellence.

Amin Sukhiani – Chief Financial Officer

Mr. Sukhiani has 20+ years of experience in finance and has led the transformation of a microfinance institution into a digital bank. He has served at Bank Alfalah, MCB, Faysal Bank, and PWC. A Chartered Accountant and ICAP Gold Medalist, he has expertise in IFRS, digital banking strategy, and corporate finance.

Shahzad Khan – Head of Channels, Lending & Corporate

With over 20 years in telecom and banking, Mr. Khan leads Easypaisa’s lending and corporate channels. He has worked with Vodafone Qatar, Mobilink, and Pepsi. His expertise includes strategy, performance management, and financial modelling.

Farhan Hassan – Head of Wallet Business

With over 15 years of experience, Mr. Hassan oversees Easypaisa’s Wallet Business, covering payments, savings, lending, and mini app platforms. He has worked with Telenor and China Mobile across Asia and Europe. His focus is on developing customer-centric digital products and fostering growth.

Muhammad Khurram Warraich – Head of Digital Lending & Data Science

Mr. Warraich has 19 years of experience in digital lending, analytics, and business strategy. He has worked with HBL, Mobilink, and Telenor. He is among the early contributors to digital lending innovation in Pakistan.

Muhammad Rizwan Ikram– Chief Risk Officer

With 22+ years in risk management, Mr. Ikran has worked across ERM, credit, market, and operational risk domains. He played a founding role in Mobilink and U Microfinance Banks. His expertise includes credit administration, process re-engineering, and information security risk.

Mohammad Hasan Ayaz – Chief Technology Officer

With 17 years in fintech and telecom, Mr. Ayaz leads technology strategy and operations. He has managed large-scale tech programs with a focus on governance, architecture, and innovation.

Syed Umar Viqar – Head of Operations

Bringing 25 years of experience, Mr. Viqar has led operational and strategic roles in commercial and microfinance banks. His focus includes digitalization, automation, and reducing transaction turnaround time. He has served with Standard Chartered, Dubai Islamic Bank, and Mobilink Microfinance Bank.

Pouruchisty Sidhwa – Chief Human Resource Officer

Ms. Sidhwa brings 20+ years of HR, finance, and risk experience from firms like CITI, RBS, and Shan Foods. She is skilled in aligning people strategy with business goals and managing large employee bases. She is also a certified coach.

Kashif Ahmed – Chief Compliance Officer

Mr. Ahmed has 28 years of experience across compliance, audit, and operations. He has worked with MCB Islamic Bank, Deloitte, and Mashreq Bank. A Chartered Accountant, he has enhanced compliance culture and operational efficiency throughout his career.

Amna Abbas – Chief Legal Officer & Company Secretary

Ms. Abbas has 11 years of legal advisory and litigation experience. A Barrister from Lincoln’s Inn, she holds an LLM from Queen Mary University. Her expertise includes employment law, contracts, and corporate compliance.

Junaid Yusuf Kara – Chief Audit Executive

Mr. Kara has over 20 years of audit experience, with a specialization in IT audits. He has worked with KPMG, EY, RBS, and Standard Chartered. A Platinum ISACA member, he has contributed to audit literature and editorial initiatives.

Effectiveness

Easypaisa Bank has the following five management committees to effectively manage and oversee operations, details of which are as follows:

1) Management Committee, Composition:

The Management Committee is responsible for decision-making and providing recommendations on matters related to the Bank's overall strategy, management, and administration. Its scope explicitly excludes lending activities. The committee ensures alignment of strategic priorities with operational execution. 2) Asset Liability Committee (ALCO), Composition:

The ALCO conducts oversight of the balance sheet structure, product maturity profiles, risk-return alignment, and implications for profitability. The committee also reviews and approves new and existing bank products + pricing and reviews investment strategies, treasury portfolio and market risk parameters, while ensuring compliance with regulatory guidelines, interest rate risk, and liquidity risk policies and associated procedures. 3) Management Risk Committee (MRC), Composition:

The MRC oversees the identification, assessment, and management of material financial and non-financial risks across the Bank’s operations. The committee evaluates key risk exposures and ensures appropriate risk mitigation frameworks are in place to support the Bank's risk appetite and regulatory expectations. 4) Compliance Committee (CCM), Composition:

The CCM monitors and oversees the Bank’s compliance risk at an enterprise level. It ensures effective resolution of cross-functional compliance issues, including those that are self-identified or reported. The committee strengthens the Bank’s control environment and promotes a culture of compliance throughout the organization. 5) IT Steering Committee (ITSC), Composition:

The ITSC provides strategic oversight of the Bank’s information technology landscape. It comprises members with both technical and functional expertise to guide decision-making on IT initiatives, evaluate technology investments, and align IT strategy with business goals. The committee also facilitates IT - CAPEX planning and supports technology enablement across functions.

MIS

The BI data warehouse serves as the backbone of analytics in Easypaisa Digital Bank, enabling data-driven decision-making at all levels. It provides daily automated insights on core financial activities, including disbursements, repayments, recoveries, and deposits. Segmented reporting across branch and branchless channels offers a clear view of operational performance. These business-critical dashboards help align execution with strategic priorities. BI ensures accurate, consistent, and timely access to key performance indicators, empowering management to proactively drive business outcomes with precision.

Risk Management framework

The Bank has a robust Risk Division Unit tasked with overseeing risks associated with the Banking in general and specifically the risks associated with Digital Banking. The Bank has meticulously developed and deployed a comprehensive credit policy, which encompasses guidelines for its Credit risk management framework. On top of that, the Bank has successfully developed and deployed an in-house system to assess customers’ credit history and evaluate their credit scores to make more informed lending decisions. To further strengthen its risk posture, the Bank has adopted a forward-looking approach to credit risk management through the implementation of IFRS 9, transitioning to an expected credit loss (ECL) model. This enhances the Bank’s ability to anticipate potential credit losses and maintain a more accurate reflection of its financial health.

In parallel, the Bank continues to invest in Cybersecurity and data protection. With a focus on continuous monitoring, encryption, and strict access controls, these measures form a multi-layered defense strategy to mitigate emerging cyber threats, ensure regulatory compliance, and uphold operational integrity in an increasingly digital financial landscape.

As a digital bank, the bank is prioritizing Digital wellbeing and Cybersecurity across infrastructure, customer interfaces, and service-supporting assets. The bank has implemented robust solutions to enhance our cybersecurity posture and monitoring capabilities while investing significantly in data privacy to meet regulatory requirements and public expectations. The commitment is validated through PCI-DSS (4.0) and ISO 27001 certifications, providing stakeholders with added assurance

In addressing information and cybersecurity concerns, the bank has prioritized combating Digital Frauds and Scams since 2021. The enhanced processes and services have successfully reduced customer exposure to fraudulent activities. The bank remains committed to full compliance with SBP regulatory requirements for Digital Banking Products and Services security while implementing industry best practices. The ongoing collaboration with Ant International has been instrumental in developing these capabilities, and the bank continues to strengthen fraud management framework.

Risk Management effectiveness depends critically on data quality and analytics capabilities. The bank has a robust Risk Analytics function that leverages MIS to deliver timely, detailed operational insights enabling calculated management decisions. The bank is enhancing these capabilities through planned automation and AI implementation to generate enterprise-level insights for comprehensive risk management across the organization.

Technology Infrastructure

Easypaisa Bank Limited is Pakistan’s first digital bank, powered by the robust Ericsson’s Wallet Platform for digital servicing and T24 for core banking product suit. It delivers seamless financial services to customers through a unified, secure platform handling over 10,000 TPS and 400M monthly transactions

The bank offers one of the fastest account opening experiences and a comprehensive digital journey for users. The tech stack is among the most scalable and resilient in the country’s financial ecosystem and Easypaisa Super App provides an one stop shop experience from payments and savings to lending and deposits and all other embedded financial services. This ensures accessibility, performance, and financial inclusion at scale. In line with its transition to a “digital first” strategy, the Bank has streamlined its physical footprint by reducing its branch network to 25 locations, transforming the remaining branches into cashless service centers. This shift supports its evolution into Pakistan’s first fully digital retail bank, offering customers a more seamless and efficient banking experience.

Business Risk

Industry Dynamics

In January 2023, the State Bank of Pakistan (SBP) issued No Objection Certificates (NoCs) to five applicants: Easypaisa, HugoBank Limited, KT Bank Pakistan Limited, Mashreq Bank Pakistan Limited, and Raqami Islamic Digital Bank Limited. These institutions were subsequently granted In-Principle Approval (IPA) in September 2023 to begin preparations for operational readiness, marking a significant step toward the development of digital banking in Pakistan. By January 2025, Mashreq Bank Pakistan Limited received a restricted license from the SBP to initiate pilot operations as a digital retail bank. Easypaisa, with its operational history and well-designed business strategy, was exempted from pilot testing requirements and restrictions on limited deposit-taking. It was granted a full Digital Retail Bank License in January 2025. As the digital banking ecosystem evolves, traditional commercial banks are also transforming by embracing digital technologies, forging partnerships with fintech companies, and prioritizing customer experience. They are increasingly leveraging digital platforms to broaden their reach, boost operational efficiency, and offer more competitive financial solutions, allowing them to effectively compete with emerging digital banks. Looking ahead, key challenges will include safeguarding customer data, maintaining adequate liquidity to meet digital demand, and ensuring compliance with rapidly evolving regulatory requirements.

Relative Position

Easypaisa was one of five contenders for a digital retail bank license under Pakistan’s Digital Banks Framework 2022, committed to financial inclusion. The successful transition from microfinance banks to digital retail bank, marks a defining moment in the Bank’s journey, reaffirming its position as a leader in Pakistan’s digital landscape.

Revenue

During CY24, the markup income of the Bank increased by 59% and stood at PKR 25.9bln (CY23: PKR 16.3bln) due to higher earnings from advances and investments. However, markup expenses increased by 43% to PKR 1.49bln (CY23: PKR 1.04bln) because of increased deposit expenses. Consequently, the Net Interest Margin (NIMR) inclined by 60% and was reported at PKR 24.4bln (CY23: PKR 15.3bln).

Profitability

In CY24, the Non-markup income grew by 37.6% to stand at PKR 14.5bln (CY23: PKR 10.5bln), mainly due to the fee and commission income, which stood at PKR 14.4bln. The Profit After Tax (PAT) of the Bank significantly inclined by 580% and was reported at PKR 3.4bln (CY23: PKR 0.5bln), primarily driven by a strengthened topline and exceptional growth in income from branchless banking.

Sustainability

With Telenor Group as the major 55% shareholder and Ant Financial Services Group holding 45% of Easypaisa's shares, the Bank is committed to creating long-term sustainable shareholder value. As one of the largest branchless banking service platforms in the country, the Bank's platform is geared towards delivering the best user experience through a comprehensive suite of innovative products for payments, deposits, and lending tailored to the needs of its valued customers.

In January 2025, Easypaisa Bank Limited reached a historic milestone by receiving the country's first-ever Digital Retail Bank License, making it the first digital bank to gain commercial launch approval in Pakistan. This achievement reflects the Bank’s pioneering role in transforming the financial sector and marks a major step toward enhanced financial inclusion and digital innovation. With this license, Easypaisa is set to expand beyond its mobile wallet offerings, providing a full range of digital banking services—including deposit accounts, credit cards, digital loans, investment products, and insurance—through a secure and user-friendly app. This development reinforces the commitment to empowering fintech innovation and increasing access to financial services for underserved populations across the country. .

Financial Risk

Credit Risk

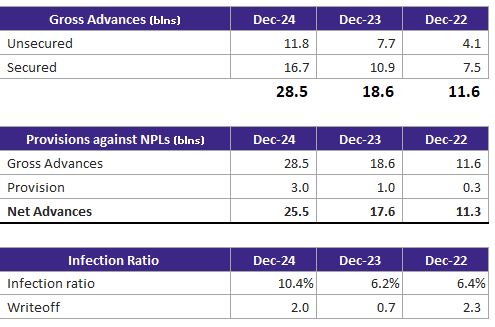

At end-Dec24, the Bank’s net advances increased by 45% to PKR 25.5bln (end-Dec23: PKR 17.6bln), with Non-Performing Loans (NPLs) increasing to PKR 2.9bln (end-Dec23: PKR 1.1bln). Consequently, the infection ratio rose to 10.4% (end-Dec23: 6.2%). At end-Dec24, the net advances to deposit ratio (ADR) of the Bank stood at 33.5% (end-Dec23: 34.5%). The Provisioning Expenses increased to

PKR 2.7bln (end-Dec23: PKR 0.5bln). This increase was primarily driven by the adoption of the IFRS-9 and significantly higher digital lending disbursements. In 2024, Digital Lending disbursements grew by 3x to PKR 64bln (end-Dec23: PKR 21bln).

Market Risk

At end-Dec24, the Bank’s investment portfolio increased by 2X to PKR 60.8bln (end-Dec23: PKR 28.6bln). The investment portfolio of the Bank comprises government securities only and classified as held for sale and collect.

Funding

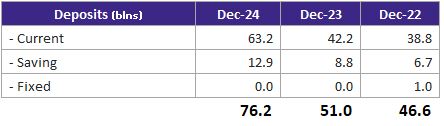

At end-Dec24, the total deposits of the Bank increased by 50% to stand at PKR 76.2bln (end-Dec23: PKR 50.9bln), CASA stood at 99.9% and CA stood at 83% highest in the financial industry, and resultantly the lowest cost of deposits (1.8%).

Cashflows & Coverages

In Oct'24, the Bank received an equity investment of USD 10mln from its shareholders, Telenor Pakistan B.V. and Alipay (Hong Kong) Holding Limited. This capital infusion reflects the ongoing commitment of both shareholders to enhance digital services and promote financial inclusion in Pakistan.

Capital Adequacy

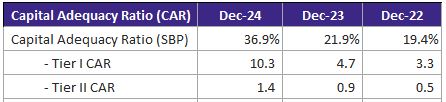

At end-Dec24, the equity base increased to PKR 14.1bln (end-Dec23: PKR 8.0bln), attributable to capital injection from the sponsors.

Consequently, the Capital Adequacy Ratio (CAR) as per MFB regulations increased to 36.9% (end-Dec23: 21.9%).

|